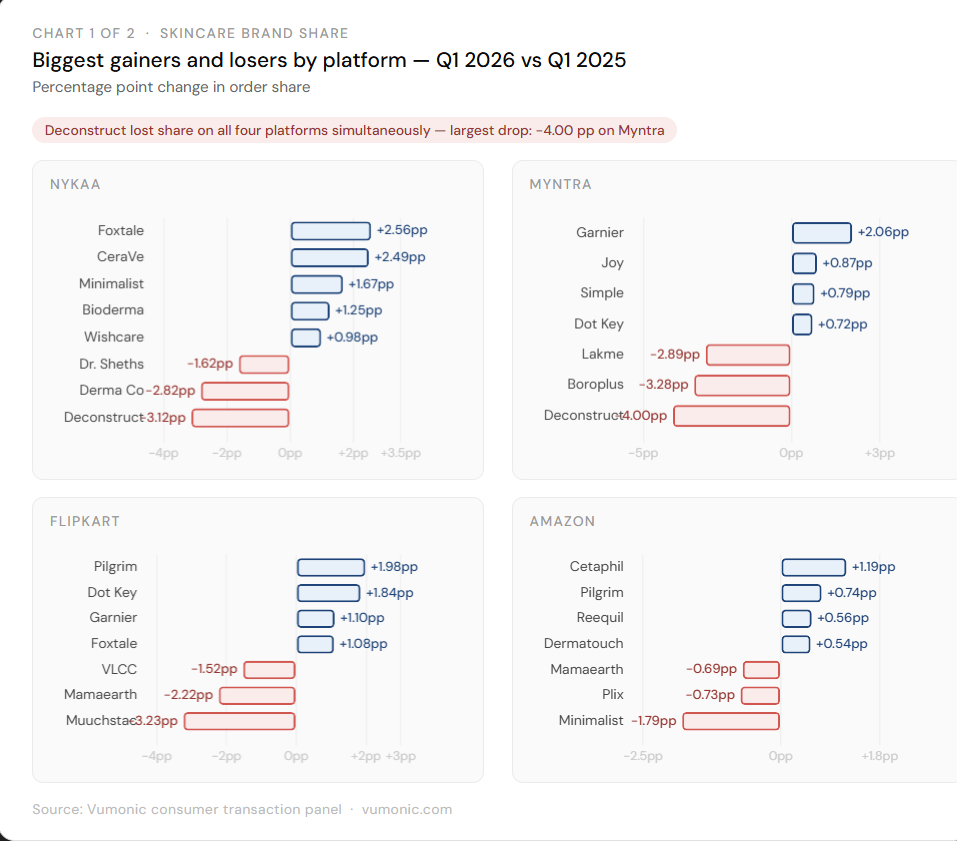

Deconstruct lost 4.00 pp on Myntra, 3.12 pp on Nykaa, 1.29 pp on Amazon, and 1.04 pp on Flipkart in Q1 2026. The same brand, losing share on every platform at the same time.

Key metrics

Biggest gainer overall: Foxtale on Nykaa, +2.56 pp YoY

Biggest single-platform loser: Deconstruct on Myntra, −4.00 pp YoY

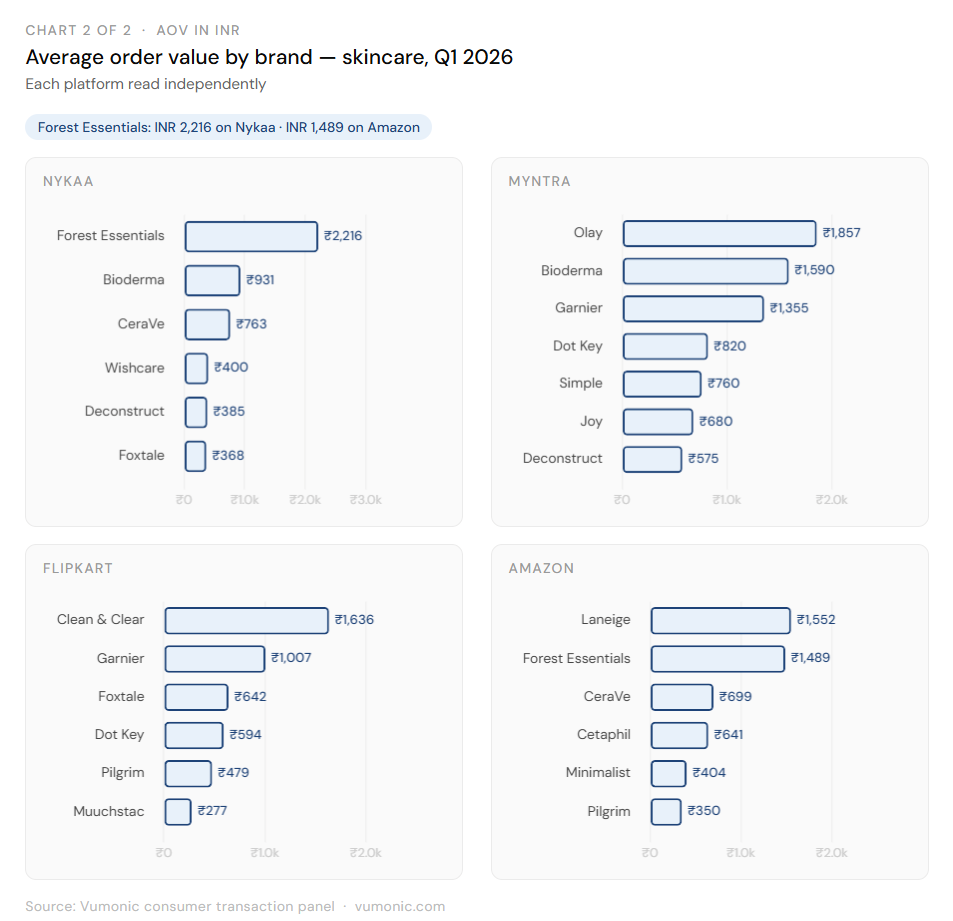

Highest AOV brand on Nykaa: Forest Essentials, INR 2,216

Highest AOV brand on Myntra: Olay, INR 1,857

3.1

Nykaa — domestic science-led D2C is losing ground at both price ends

Gainers: Foxtale +2.56 pp · CeraVe +2.49 pp · Minimalist +1.67 pp · Bioderma +1.25 pp

Losers: Deconstruct −3.12 pp · The Derma Co −2.82 pp · Dr. Sheths −1.62 pp

AOV split among gainers: CeraVe INR 763 · Bioderma INR 931 · vs Foxtale INR 368 · Wishcare INR 400

Share is growing at both the clinical/international end and the affordable functional end

Deconstruct, The Derma Co, Dr. Sheths - all three are ingredient-transparency brands that led Nykaa through 2024. They are being squeezed from above and below simultaneously.

Myntra - Deconstruct's collapse is the single largest brand share loss in this dataset

Gainers: Garnier +2.06 pp (AOV INR 1,355) · Joy +0.87 pp · Simple +0.79 pp · Dot Key +0.72 pp

Losers: Deconstruct −4.00 pp · Boroplus −3.28 pp · Lakme −2.89 pp

Deconstruct fell from 5.59% to 1.59% share in one year on Myntra

The gainers - Garnier, Joy, Simple - are widely distributed, multi-use brands with broad recognition. Not specialist skincare.

Minimalist dropped only 0.18 pp on Myntra vs Deconstruct's 4.00 pp. The ingredient-transparency category is not collapsing uniformly - Deconstruct is an outlier, not a category trend.

Flipkart - the previous category leader lost 3.23 pp in a single year

Muuchstac held 9.18% share in Q1 2025. It finished Q1 2026 at 5.95%.

Also losing: Mamaearth −2.22 pp · VLCC −1.52 pp

Gainers: Pilgrim +1.98 pp · Dot Key +1.84 pp · Foxtale +1.08 pp

AOV of gainers: Dot Key INR 594 · Foxtale INR 642 - not cheap brands replacing a cheap brand

Share dispersed across four challengers. No single brand absorbed Muuchstac's drop.

Amazon - derma-endorsed brands gaining, high-visibility D2C compressing

Gainers: Cetaphil +1.19 pp (AOV INR 641) · Pilgrim +0.74 pp · Reequil +0.56 pp · Dermatouch +0.54 pp

Losers: Minimalist −1.79 pp · Plix −0.73 pp · Mamaearth −0.69 pp

Minimalist at 7.00% still leads Amazon. It has lost share for two consecutive years.

The four gainers are all derma-positioned or clinically endorsed. The three market share losers built share through visibility and pricing.

3.2

The takeaway

Nykaa is the only platform where premium-priced brands are gaining share rather than losing it. The domestic D2C brands shedding share on Nykaa have not found a platform where they are recovering it. Deconstruct's simultaneous losses across all four platforms make that point most clearly: this is not a platform-mix problem, it is a brand positioning problem playing out everywhere at once.