16

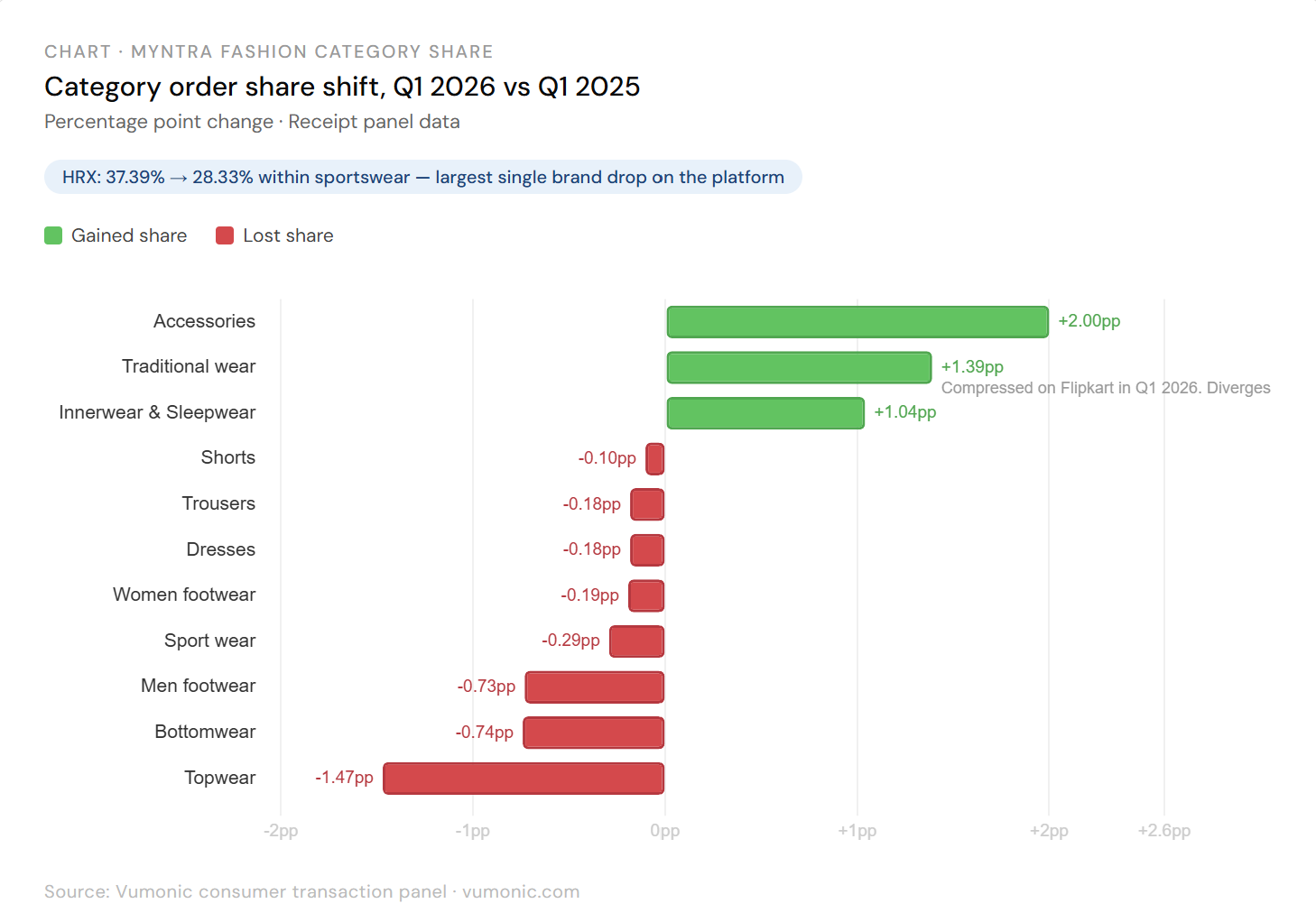

HRX held 37.39% of sportswear orders on Myntra in Q1 2025. By Q1 2026 that had fallen to 28.33%, a 9.06 pp drop in a single year. No single brand absorbed the gap. Puma reached 4.46%, Glitchez entered the top five at 4.29%, Technosport appeared at 2.75%. The top of Myntra's sportswear category looks nothing like it did twelve months ago, and no challenger has consolidated.

Sportswear's overall category share barely moved, down just 0.29 pp to 3.36%. The buyers stayed. The brands they chose changed.

Bottomwear shows the same pattern. Highlander dropped from 10.61% to 3.87% brand share within the category, a 6.74 pp fall. Roadster, the category's longest-standing leader, fell from 14.09% to 11.85%. Levi's slipped from 5.89% to 3.67%. Three established names losing ground at the same time, with Glitchez and H&M entering the top five from outside it. Bottomwear's category share compressed 0.74 pp to 12.88% and median AOV held near-flat at INR 1,300.

Traditional wear moved in the opposite direction. It grew 1.39 pp to 14.41% of Myntra fashion orders. Within the category, Anouk extended its lead from 11.66% to 13.61%. Libas fell from 7.20% to 4.42% and House of Pataudi entered at 3.88%. One brand consolidating while challengers rotate. This cuts directly against what Flipkart showed in Q1 2026, where traditional wear contracted 0.92 pp. The divergence is platform-specific, not category-wide.

Accessories crossed 14.60% of fashion orders, up 2.00 pp. SZN entered the top rankings at 5.91% to become the category's new leader. Roadster fell from 4.81% to 3.67% and Fastrack dropped out of the top five. Median AOV in accessories fell from INR 1,378 to INR 1,211.

Topwear is still 40.80% of all Myntra fashion orders. Roadster's share within it fell from 16.83% to 14.38%, Highlander from 6.23% to 3.73%, and Glitchez entered at 3.44%. Category share, not collapsing. Brand order within it, quietly reorganising.

Repeat rate on Myntra fashion rose from 48.52% to 51.61%. Average orders per active user per month moved from 1.70 to 1.80. The buyer base is more active than a year ago. Sportswear and bottomwear have open slots at the top of their brand tables, in a growing environment. Neither category has a clear consolidating challenger yet.

Tags: Fashion · Myntra · Q1 2026 · Consumer panel data · D2C brands

Want a custom cut of this data for your brand? Get in touch with the Vumonic team at vumonic.com